Visualizing external fundraising and donations in universities and research and development institutions

Analysis of status of external fundraising and donations

Visualizing external fundraising and donations in universities and research and development institutions

Analysis of status of external fundraising and donations

1. Purpose of “visualization”

As a part of the EBMgt of universities and other entities, this survey examines the virtuous cycle of funding indicated in the Guidelines for Enhancing Industry–University Collaboration Activities (enacted on November 30th, 2016; hereafter, “guidelines”). This study visualizes the status of external funding and donations, which have recently become important revenue streams for these corporations from the perspective of “optimizing cost allocation for industry–university” and “enhancing corporate financing for universities and national research and development institutions,” in order to provide organized evidence to contribute to improving EBMgt.

Specifically, the percentage of external public funding with a high degree of spending flexibility and donations within the entirety of corporate financing and current high-growth finances, joint research, and donations are visualized. In addition, amid corporations’ efforts to deal with indirect costs (especially joint research revenues) from the perspective of optimizing cost allocation, the indirect cost ratio and incoming revenue of each corporation have been visualized, and their contributions to overall finances are analyzed. Furthermore, donations have been divided according to source types (corporate or individual) and the contributions visualized.

2. “Visualization” method

2.1. Overview of this study

- 【Objects】 Subjects, measures, and target institutes of this study

- 【Questionnaires】 Questionnaire drafting and trial analysis

- 【Implementation】 Questionnaire dissemination, collection, sending reminders, and data-input

- 【Analysis and sharing】 Data aggregation, interviews, interpretation, and the dissemination of outputs for relevant ministries and government agencies

2.2. Viewpoints

- 【Viewpoint 1】 Importance of external funding and indirect costs in corporate finances

- 【Viewpoint 2】 Shifts in joint research income and indirect costs

- 【Viewpoint 3】 Shifts in donation revenues

2.3. Study subjects and source of information

- Financial statements of national university corporations

- The Cabinet Office’s “Survey of industry–university collaboration activity management”

Questionnaire for national research and development institutions (PDF)

Questionnaire for national research and development institutions (PDF) - The Cabinet Office’s “Survey of industry–university collaboration activity management” Questionnaire for national university corporations(PDF)

- The Ministry of Education, Culture, Sports, Science and Technology’s (MEXT) “Survey on the status of implementation of industry–university collaboration at universities and relevant institutes”

2.4. Duration of Survey

- April 2019 to March 2020

2.5. Study implementation

- The Director General of Science, Technology and Innovation from the Cabinet’s Office

- Title of contract: Survey on the enactment status of guidelines for cash flow management by national university corporations, inter-university research institute corporations, and national research and development institutions

- Contractor: educe Co., Ltd.

2.6. Institutes targeted by this study

| Source of information | National university corporations (including inter-university research institute corporations) | Public and private universities | National research and development institutions |

| Financial statements | 90 institutes | – | 29 institutes |

| The Cabinet Office’s “Survey on industry–university collaboration activity management”* | 68 institutes | 68 institutes | 26 institutes |

| MEXT’s “Survey on the status of implementation of industry–university collaboration at universities and relevant institutes” | 88 institutes (Viewpoint 2) 90 institutes (Viewpoint 3) | 303 institutes (Viewpoint 2) 550 institutes (Viewpoint 3) | – |

*Organization names are not disclosed because the industry–university collaboration evaluation index data compiled from the Cabinet Office’s surveys are collected under the premise that individual responses will not be disclosed to the public in any form, although analysis indicating the actual names of institutes is required for improving performance by referencing best practices. Hence, organizations participating in this study are allowed to use other analysis tools with their actual names. This is only available to organizations that provide permission for their information to be shared among participating organizations. Furthermore, out of the 162 institutes that responded (excluding Technology Licensing Organizations, hereafter TLOs), 157 institutes (97%) indicated that their data could be shared among participants.

2.7. Notes

2.7.1. Terminology in analysis items

- ・ Indirect cost ratio: the amount of indirect costs received/direct costs

- ・ Total indirect costs: the sum of indirect costs from consignment research, joint research, consignment projects, grants-in-aid for scientific research, and subsidies

- ・ School-related revenues: tuition, admission fees, and examination fees

- ・ External funding revenues: amount of consignment research received, amount of joint research received, amount of consignment projects received, grants-in-aid for scientific research received, amount of donations, and other subsidies

- ・ Amount of donations received: amount of cash donations received

3. “Visualization” results

3.1. 【Viewpoint 1】 The importance of external funding and indirect costs in corporate finances

The government has set a goal of trebling private funds to build corporate financing. It is particularly important to increase indirect cost revenues that have a high degree of spending flexibility. For Viewpoint 1, the importance of consignment research, joint research, grants-in-aid for scientific research, and donations in external funding for corporations, including private funds, are visualized. This is followed by a comparison of indirect costs in external funding, which may be used with relatively large flexibility and total general administrative expenses. * However, as stated above, in this visualization, organization names from Cabinet Office surveys are not disclosed, and institute names are only shown for results obtained from public data, including the financial statements of national university corporations and organizations’ websites.

Analysis items

- 【1-1】The component ratio of external funding revenue and the amount of donations received in revenues (FY 2018) of national university corporations, inter-university research institute corporations, and national research and development institutions.

- 【1-2】Breakdown of direct and indirect costs in external funding revenue, and the amount of donations received (FY 2018) for national university corporations, inter-university research institute corporations, and national research and development institutions.

- 【1-3】Breakdown of the amount of indirect costs received (FY 2018) for national university corporations, inter-university research institute corporations, and national research and development institutions.

- 【1-4】List of indirect cost ratios per external funding (FY 2018) for national university corporations and inter-university research institute corporations

- 【1-5】General financial framework (ordinary profit and loss excluding affiliated hospitals) for national university corporations and inter-university research institute corporations (FY 2018)

- 【1-6】Comparison of the “total indirect costs received” plus the “amount of donations received” and the “general administrative expenses” for national university corporations (FY 2016–2018), inter-university research institute corporations (FY 2016–2018), and national research and development institutions (FY 2018).

- 【1-7】Comparison of all amounts of indirect costs received, as well as general administrative expenses for national university corporations (FY 2016–2018), inter-university research institute corporations (FY 2016–2018), and national research and development institutions (FY 2018)

*Data for national research and development institutions are not disclosed

3.1.1. 【1-1】 The component ratio of external funding revenue and the amount of donations received in revenues (FY 2018) for national university corporations, inter-university research institute corporations, and national research and development institutions

The component ratio of the revenues of each university, inter-university research institute corporation, and national research and development agency is shown in the figure below. Corporate revenues show a dependency on external funding and donations.

Source: Financial statements of national university corporations (cash flow and detailed statements annexed)

3.1.2. 【1-2】 The breakdown of direct and indirect costs in external funding revenue and the amount of donations received (FY 2018) for national university corporations, inter-university research institute corporations, and national research and development institutions

The component ratios of external funding and the total amount of indirect costs are shown in the figure below. The visualization shows the total amount of indirect costs incurred in all external funding revenue.

Source: Financial statements of national university corporations (detailed statement annexed)

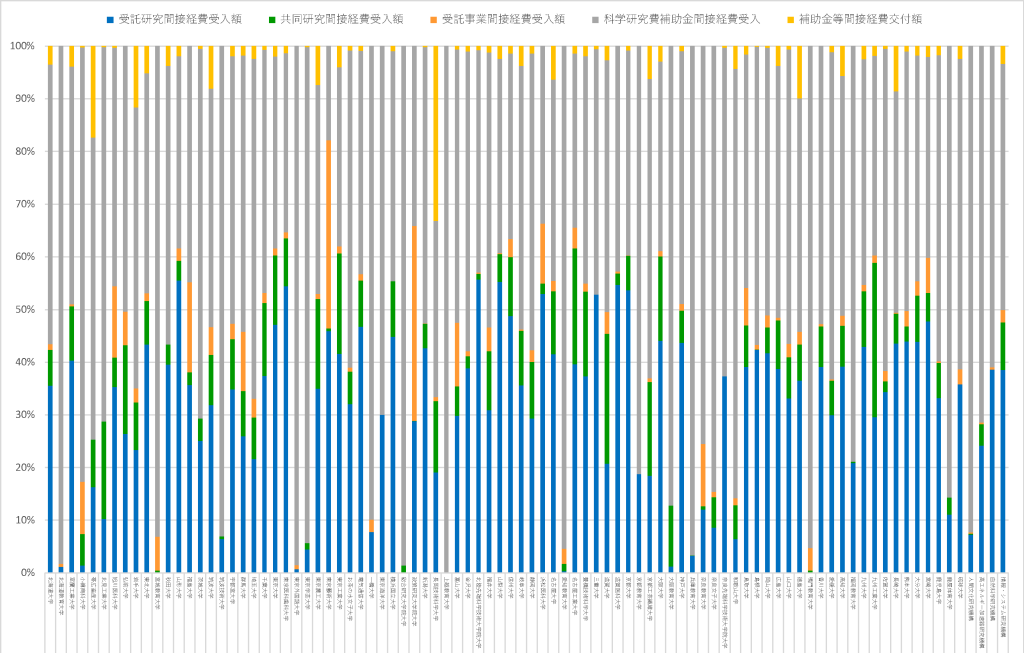

3.1.3. 【1-3】 The breakdown of the amount of indirect costs received (FY 2018) in national university corporations, inter-university research institute corporations, and national research and development institutions

The breakdown of the percentage of indirect costs received, making up the total indirect costs, is shown in the figure below. The visualization shows the funding for indirect costs that is received most often.

Source: Financial statements of national university corporations (detailed statement annexed)

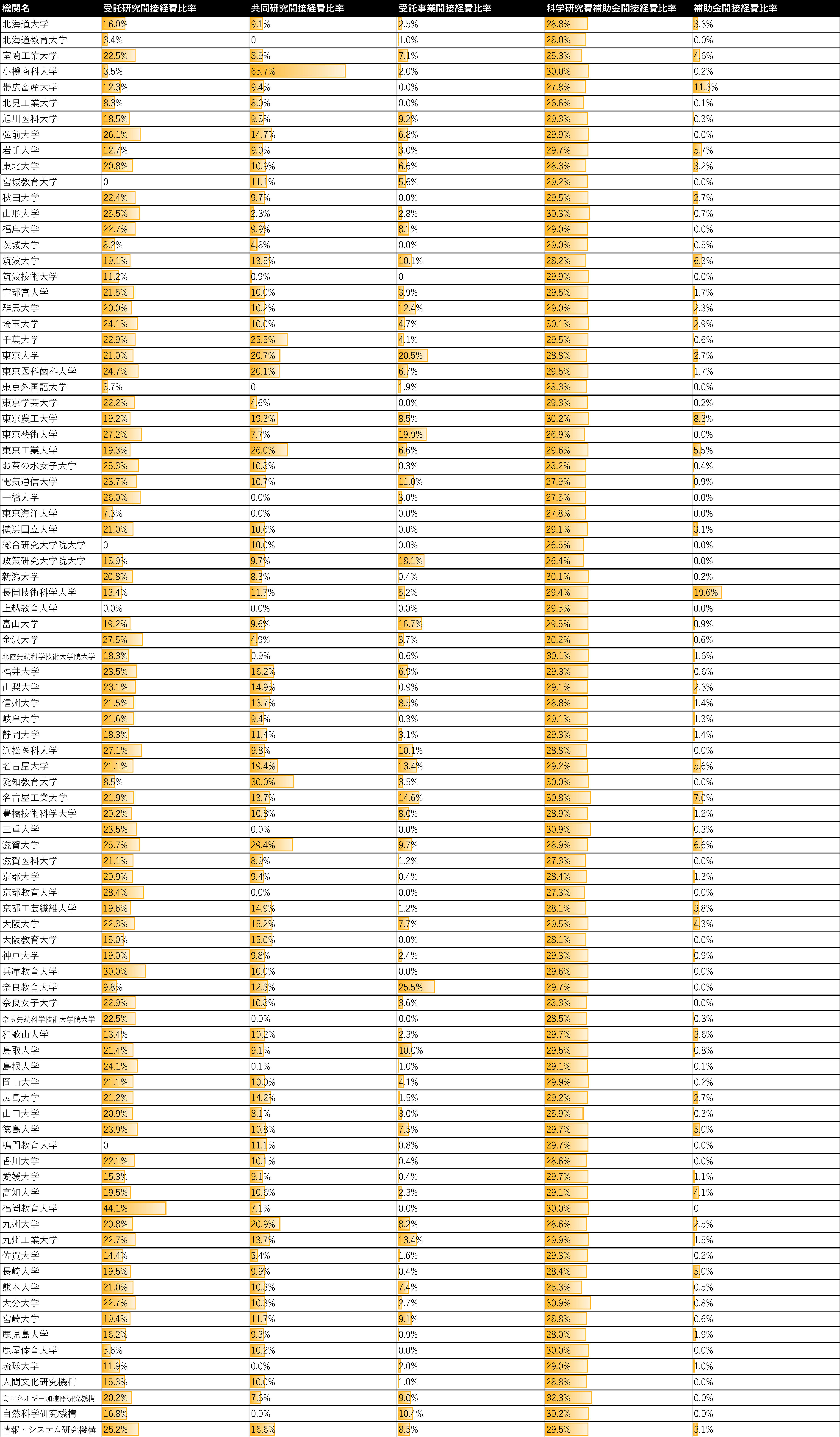

3.1.4. 【1-4】 List of indirect cost ratios per external funding source (FY 2018) of national university corporations, inter-university research institute corporations, and national research and development institutions

A comparison of the indirect cost ratios per external funding source is shown below. The visualization shows the ratio of the indirect costs associated with the external funding of each corporation (FY 2018).

Source: Financial statements of national university corporations (detailed statement annexed)

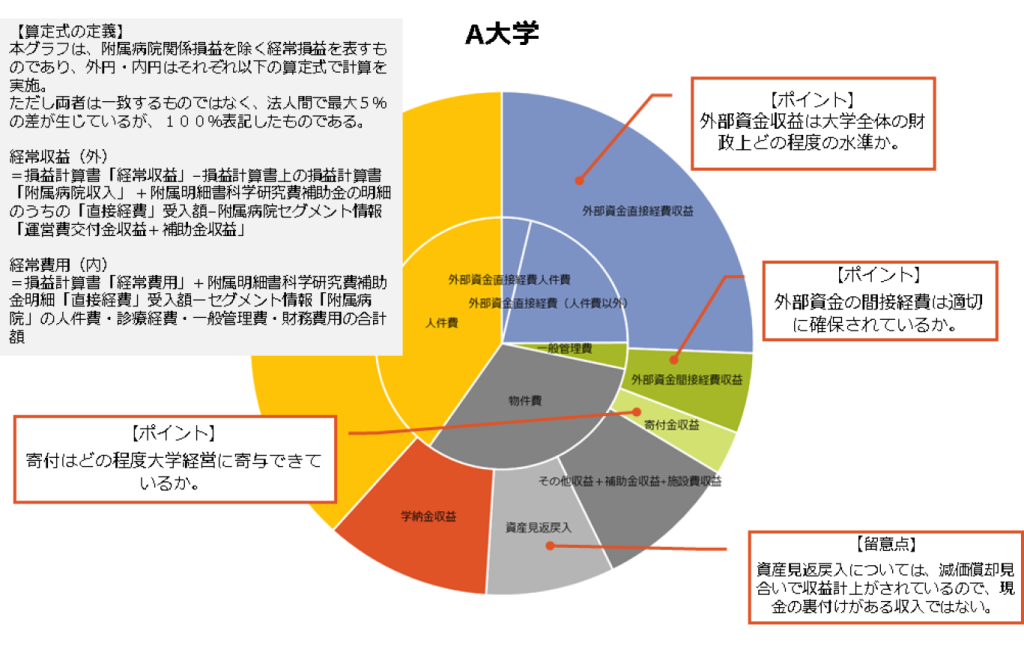

3.1.5. 【1-5】 General financial framework (ordinary profit and loss, excluding affiliated hospitals) of national university corporations and inter-university research institute corporations (FY 2018)

The contribution of external funding (consignment research, joint research, consignment projects, and grants-in-aid for scientific research) and donations, acquired for overall university finances, is presented in the figure below. The visualization shows external fundraising covers not only direct costs associated with external funding, but also general administrative expenses. *The total amount of “revenue according to profit and loss calculations” in the outer circle and “expenses according to profit and loss calculations” in the inner circle do not entirely match (both have a 5% difference at maximum).

Source: Financial statements of national university corporations and inter-university research institute corporations (profit and loss statement)

3.1.6. 【1-6】 Comparison of “total indirect costs received” plus “amount of donations received” and general administrative expenses for national university corporations (FY 2016–2018), inter-university research institute corporations (FY 2016–2018), and national research and development institutions (FY 2018)

A longitudinal comparison of the ratio between the general administrative expenses of all corporations and the total amount of all direct costs associated with external funding and donations is shown in the figure below. The visualization shows the importance of indirect costs associated with external funding and donations compared to general administrative expenses for all corporations.

Source: Financial statements of national university corporations and inter-university research institute corporations

3.1.7. 【1-7】Comparison of all amounts of indirect costs received and general administrative expenses for national university corporations (FY 2016–2018), inter-university research institute corporations (FY 2016–2018), and national research and development institutions (FY 2018)

A longitudinal comparison of the ratio between general administrative expenses of all corporations and all direct costs associated with external funding is shown in the figure below. The visualization shows the importance of indirect costs associated with external funding compared with overall general administrative expenses.

Source: Financial statements of national university corporations and inter-university research institute corporations

3.2. 【Viewpoint 2】 Transition of joint research income and indirect costs

In Viewpoint 2, a visualization of the difference in the ratio of indirect costs to direct costs in joint research, depending on the corporation and based on its relation to numbers and amounts received, is performed. The indirect cost ratio associated with joint research of many corporations has greatly changed over the past few years, and the main base rate and regulations for indirect costs are listed based on public information.

Analysis items

- 【2-1】Comparison of the amount of indirect costs received associated with joint research and general administrative expenses for national university corporations (FY 2016–2018), inter-university research institute corporations (FY 2016–2018), and national research and development institutions (FY 2018)

- 【2-2】Comparison of the amount of joint research received and indirect cost ratio associated with joint research for national university corporations (FY 2016–2018), inter-university research institute corporations (FY 2016–2018), and national research and development institutions (FY 2018)

- 【2-3】Comparison of the number of joint research projects and the amount received per joint research project for national university corporations (FY 2016–2018), inter-university research institute corporations (FY 2016–2018), and national research and development institutions (FY 2018)

- 【2-4】Rules for indirect costs associated with the joint research income of national university corporations (FY 2016–2018), inter-university research institute corporations (FY 2016–2018), and national research and development institutions (FY 2018)

*【2-3】and National research and development institutions’ data are not open to the public.

3.2.1. 【2-1】Comparison of the amount of indirect costs received associated with joint research and general administrative expenses of national university corporations (FY 2016–2018), inter-university research institute corporations (FY 2016–2018), and national research and development institutions (FY 2018)

A longitudinal comparison between the rate of general administrative expenses of all corporations and the total amount of all direct costs associated with joint research is shown in the figure below. Indirect costs associated with joint research have exhibited high growth in recent years compared to the general administrative expenses for all corporations.

Source: Financial statements of national university corporations and inter-university research institute corporations

3.2.2. 【2-2】Comparison of the amount of joint research received and indirect cost ratio associated with the joint research of national university corporations (FY 2016–2018), inter-university research institute corporations (FY 2016–2018), and national research and development institutions (FY 2018)

Shifts in the amount of joint research received and the indirect cost ratio associated with joint research are shown in the figure below. The visualization shows the changes in joint research received and indirect cost ratios over a 3-year period (FY 2016–2018).

Source: Financial statements of national university corporations and inter-university research institute corporations

3.2.4. 【2-4】Rules for indirect costs associated with joint research income (FY 2018) of national university corporations, inter-university research institute corporations, and national research and development institutions

By consulting corporate websites (as of January 31st, 2020), the status of standards established by each corporation for indirect costs associated with joint research are shown below (items not found on websites are indicated as “not provided on website”). Major changes in rules established for the indirect cost ratio of joint research income are evident from the results.

Source: Compiled by the Cabinet Office from the websites of each corporation and agency

3.3. 【Viewpoint 3】 Shifts in donation revenues

To accelerate trebling private funding, endowments, endowed courses, and endowed research, departments are also important. From this viewpoint, visualizations of donation-based revenues and the status of various donations received by national university corporations, inter-university research institute corporations, and national research and development institutions were performed.

- 【3-1】Comparison of the amount of donations received and general administrative expenses (FY 2016–2018) forof national university corporations, inter-university research institute corporations, and national research and development institutions

- 【3-2】Comparison of the amount of donations received and donation overhead rate (FY 2018) forof university corporations (national, public and private)), and national research and development institutions

- 【3-3】Comparison of the number of donations and amount of donations received byof university corporations (national, public and private) (FY 2016–2018)), and national research and development institutions (FY 2018)

- 【3-4】Comparison of the number and amount of donations from corporations (FY 2018) toward university corporations (national, public and private) and national research and development institutions

- 【3-5】Comparison of the number of donations and amount of donations from individuals (FY 2018) towardof university corporations (national, public and private)), and national research and development institutions

- 【3-6】The amountAmount of donations received per donation source (corporate and individual) (FY 2018) byof university corporations (national, public and private)), and national research and development institutions

- 【3-7】The division of endowed and non-endowed funds from the amount of donations received (FY 2018) by university corporations (national, public and private) and national research and development institutions

* In 【3-2】 and 【3-3】, FY 2016 and 2017 data from university corporations (national, public and private) are not disclosed. Similarly, in 【3-4】 to 【3-7】, data from national research and development institutions are not disclosed either.

3.3.1. 【3-1】Comparison of the amount of donations received and general administrative expenses (FY 2016–2018) for national university corporations, inter-university research institute corporations, and national research and development institutions

A longitudinal comparison of the ratio between donations received by each corporation and general administrative expenses for all corporations and agencies is shown in the figure below.

Source: Financial statements of national university corporations and inter-university research institute corporations

3.3.3. 【3-3】Comparison of the number of donations and amount of donations received byof university corporations (national, public and private) (FY 2016–2018)), and national research and development institutions (FY 2018)

A longitudinal change in the amount and number of donations is shown in the figure below. The visualization shows the changes and trends in the amount and number of donations for each institute.

Source:MEXT, “Survey on theof status of implementation of industry–university collaboration at universities (including junior colleges), colleges of technology, and inter-university research institute corporations”

4. Material

The above reports can be obtained in pdf format.

- TOP

- Visualizing external fundraising and donations in universities and research and development institutions

- Analysis of status of external fundraising and donations